Contents

This blog is a guest post by our partners at RingCentral.

It’s easy to overlook how much technology has changed our day-to-day lives. Until you take a step back and think about the norms of even a few years ago, you don’t appreciate how far things have evolved. Across every niche and field, we as consumers increasingly demand things on our own terms.

The banking industry is far from exempt from new consumer expectations. Banks and other financial institutions are having to adapt at a rapid pace. Like all other businesses, customers expect to be able to access digital services. As a result, mobile banking and other technologies are driving a profound change in banking and the customer relationship.

Banking & The Customer Relationship

Traditional banking is built on relationships. In the case of small, medium, and large businesses, the connection with their local branch was one of their most important professional relationships. Face-to-face interactions and conversations were the cornerstone of the customer relationship in banking.

In recent years, technology has developed to give banking customers new options. Rather than visiting a local branch, it’s now much easier to interact with their bank remotely. Online-based transactions and communications are becoming the norm. Industry analyst, CACI, found that 22 million people managed their current accounts on their phones in 2017, in the UK alone. By 2023, the same analyst predicts that fully 72% of the UK’s adult population will bank via an app.1

The trend towards a more digital relationship is clear. Almost every major bank now offers a mobile banking app. Most banks use a VoIP phone system in their customer call centers. Many have also adopted other technologies, like AI-driven financial chatbots. A consequence of this move is the closure of small branches. This further perpetuates the move towards digital banking.

The rise of mobile banking, though, isn’t a trade off. Customers who interact with their bank digitally have the same expectations as if they walked into a branch or called a hotline. Banks have had to account for those expectations.

How Mobile Banking is Driving Change

A survey of financial professionals found that 86% saw ‘banking beyond the branch’ as a top priority.2 That means digital payments, mobile apps, and other online interactions. The banking industry, then, understands these demands. In what ways, though, is mobile banking redefining that relationship?

Customer Engagement & Retention

Mobile banking doesn’t only give customers the option to make payments on the go. For many people, it replaces any and all other interactions with their bank. Before online and mobile banking, professional customer service provided via branch staff was vital. Building rapport and trust through face-to-face interaction was how banks engaged customers. It also played a vital role in keeping the business of those customers.

A key component of the current customer relationship is digital. That means banks are having to provide a smooth online customer service. To that end, a few of the top institutions are using real-time mobile messaging or marketing.

The service provided by a banking app is improved by such messaging and marketing. It lets banks present customers with intelligent suggestions of products and services. Those suggestions come from tracking each user's finances and their use of the app.

That can help to reduce old-fashioned, friendly in-branch chats — the sort of conversations that may also have led to individual recommendations and advice. Real-time messaging and marketing change the complexion of mobile banking apps. It moves them from offering a passive service to being an interactive marketing tool.

Click-to-call functionality in apps can boost customer engagement further too. Banks can also track calls and assess engagement with messages using call tracking platforms integrated with CRM systems or other analytics suites. That kind of reporting lets them continually tweak and improve customer experience.

Deeper Integration & Collaboration

One of the main factors to explain the rise of mobile banking is convenience. Banking customers expect to be able to access services at the click of a button. One way that this may develop still further in the coming years, is through integration with other third-party apps. A main banking app, for instance, may be able to sync with a separate payroll or accounting system.

This is a further way for banks to give greater flexibility to their customers. It would allow individuals to mix and match individual financial solutions as they see fit. All without having to open separate accounts or operate distinct systems.

Such collaboration doesn’t come without challenges, however. Most mobile operating systems discourage the linking of applications on the grounds of data protection. If - and when - greater third-party integration with banking apps does develop further, security has to be a major concern for any provider.

Immediacy & Real-Time Control

Neither small businesses nor personal banking customers want to wait for financial information. A monthly statement to see what’s going on with their money doesn't cut it. Banking customers with investment portfolios, too, demand instant visibility.

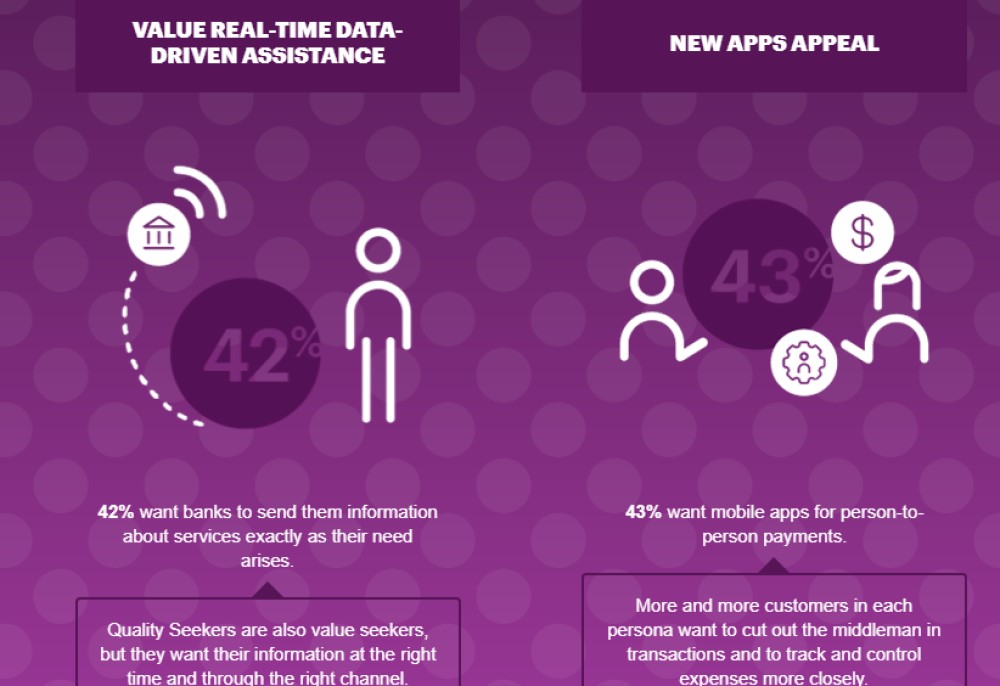

Accenture carried out a wide-ranging study into modern banking customers in 2017. They examined almost 33,000 customers across 18 markets. The results allowed them to segment respondents into categories. The category Accenture labelled ‘Quality Seekers’ made up 44% of respondents.

‘Quality Seekers’ were banking customers driven most by ideas of service and trust. They want to find a trustworthy bank with good customer service and stick with that institution. The study found that real-time data-driven assistance was particularly important to them.

As well as real-time visibility, customers also need to be able to take instant action. Customers now expect more than just bank to bank transactions to be instantaneous. They want to be able to make international payments to the same short timeframes. They need new accounts to open or investment choices to be actioned straight away. Those things now need to be part and parcel of the new customer relationship in banking.

Personalisation, Analytics & The Potential of AI

Redefining the customer relationship in the banking field isn’t straightforward. The personal touch offered by face-to-face interaction no longer plays a primary role. At least not for most banking customers. At the very highest level, for customers with the largest balances or portfolios, physical interactions are still common. Most of us, though, don’t fall into that category.

Modern digital banking customers do still expect some personalisation from their banks, however. They expect banking apps to feature tools that help them to budget, for instance. They don’t want generic advice, though. They want an app to assess their finances and offer useful guidance.

Banks are having to leverage even more cutting-edge technology to meet those demands. More specifically, they're turning to artificial intelligence (AI).

AI is the tech that can deliver the real-time data-driven insights that customers want. Through machine learning, financial institutions can create banking-specific AI tools. Those tools can collect and analyse customer account activity. They can then pinpoint important events and patterns in customer spending. That lets them develop product and service recommendations accordingly.

Eran Livneh is the VP of Marketing at AI solutions firm Personetics. She recently talked about the Royal Bank of Canada's use of an AI-based budgeting tool:

“Royal Bank of Canada recently launched an AI-powered budgeting tool that offers personalized advice to its mobile app customers…Within the first month of launching, 230,000 budgets have been set up, and customers have been able to save over $83 million total.”3

Why The Future of Banking Isn’t Digital-Only

There’s no doubt that mobile banking is on the rise. The days of individuals and businesses banking solely in-branch are well and truly over. Online banking via laptop or desktop, and especially mobile banking, are here to stay. That doesn’t mean modern banking customers fail to recognise the value of talking to a real person.

There are a few reasons why phone support remains vital to customer service in banking. First, many banking customers still don’t trust computer-only financial advice. That was another finding of the Accenture study referenced earlier. Only 19% of the study's ‘Hunters’ respondent segment trusted wholly computer-generated advice.

Phone support is still vital for customer service on a fundamental level, too. It’s a key channel through which customers can get help and support when they don’t know how to do something online. Not everyone can be tech-savvy. Older people, for instance, often need to speak on the phone for help with online transactions.

It’s not only a generational issue, though. A 2016 study by Bain & Company found that millennials call their banks more than older bankers. They called an average of 1.4 times every three months. It’s fair to say, then, that banks can’t leave phone-based customer support entirely behind.4

What’s needed is more modern phone support. The kind of support that integrates with and compliments a bank’s digital offerings. Unified Communications make this much simpler to achieve. Those setups integrate with email, analytics platforms, and other digital services.

The world’s major banks have already started to recognise the benefits afforded by modern phone support. The CEO of Citigroup, Mike Corbat, spoke earlier in 2019 about how technology can improve the customer service his firm’s call centres provide. He said:

“When you think of data, AI [artificial intelligence], raw digitisation of changing processes, we still have tens of thousands of people in call centres, and we know when we can digitise those processes we not only radically change or improve the customer experience, it costs less to provide.”5

That lets mobile banking customers enjoy the best of both worlds. They can enjoy the benefits of the modern banking customer relationship. They still, though, have real human advice to fall back on. The banks themselves, meanwhile, can more readily fold call tracking into their digital analytics. That lets them continue to improve customer experience.

Mobile Banking & A Dynamic Customer Relationship

Technological advancement makes a real difference in day-to-day life. How we all carry out those mundane tasks changes and evolves with new tech developments. Everything from retail to healthcare and travel to entertainment feels the impact. The banking industry is far from exempt.

Mobile banking is the emergent tech that has had the most significant effect on banking in recent years. Its introduction has changed not only how people bank, but also how they think about banking. It's redefining the relationship between banks and customers.

Banks must now focus far more on the digital world, and on what customers expect from them there. Institutions must cater to our increased need for instant visibility and rapid action. They must also create new digital services to aid customer engagement and personalisation.

The customer relationship in the banking niche is set to be far more fluid from now on, than ever before.

References:

1) Banking by mobile app ‘to overtake online by 2019’, BBC, (21st May, 2018)

2) Banking on relationships, Bill.com, (Aug, 2016)

3) How AI may help solve banks’ customer relationship issues, TechRepublic, (23rd Jul, 2019)

4) The Bank Brand and Call Centre Traffic Jam, Bain & Company, (Nov 29, 2016)

5) Citigroup CEO says machines could cut thousands of call centre jobs, Financial Times, (2019)

Ready to unlock real audience insight at scale?

Discover how our call intelligence will help you

Book a demo

Related posts

Categories: All Digital Marketing Interviews Marketing News PPC

1 Jul 2026 in Digital Marketing

How To Use Marketing Attribution Software to Enhance your Multi-touch Attribution Reporting

Read more

18 May 2026 in Digital Marketing

B2B Marketing Attribution Software: The Ultimate Guide for Marketers

Read more

4 Mar 2026 in Marketing Digital Marketing

Why your best leads don't convert (and how to fix it fast)

Read more

11 Feb 2026 in Marketing Digital Marketing

Call tracking software explained: ROI, support, and setup

Read more

29 Jan 2026 in News PPC Marketing Digital Marketing

Smart Outcomes: Sector specific signals for PPC optimisation

Read more

1 Jan 2026 in PPC Marketing Digital Marketing

Get more value from your marketing data in the New Year

Read more

3 Dec 2025 in Digital Marketing

Proving ROI under budget cuts – why first-party call data is the missing link

Read more

19 Nov 2025 in Digital Marketing

Wasted budget – how poor lead quality increases CPL and drags down margins

Read more

16 Jul 2025 in Marketing Digital Marketing

Call tracking glossary 2025: Essential terms for marketers

Read more